When a company borrows money, either through a term loan or a bond , it usually incurs third-party financing fees (called debt issuance costs). These are fees paid by the borrower to the bankers, lawyers and anyone else involved in arranging the financing.

Prior to April 2015, financing fees were treated as a long-term asset and amortized over the term of the loan, using either the straight-line or interest method (“deferred financing fees”).

In April 2015, FASB issued ASU_2015-03, an update that changes how debt issuance costs are accounted for. Effective December 15, 2015, an asset will no longer be created, and the financing fee will be deducted from the debt liability directly as a contra-liability:

To simplify presentation of debt issuance costs, the amendments in this Update require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts.

– Source: FAS ASU 2015-03

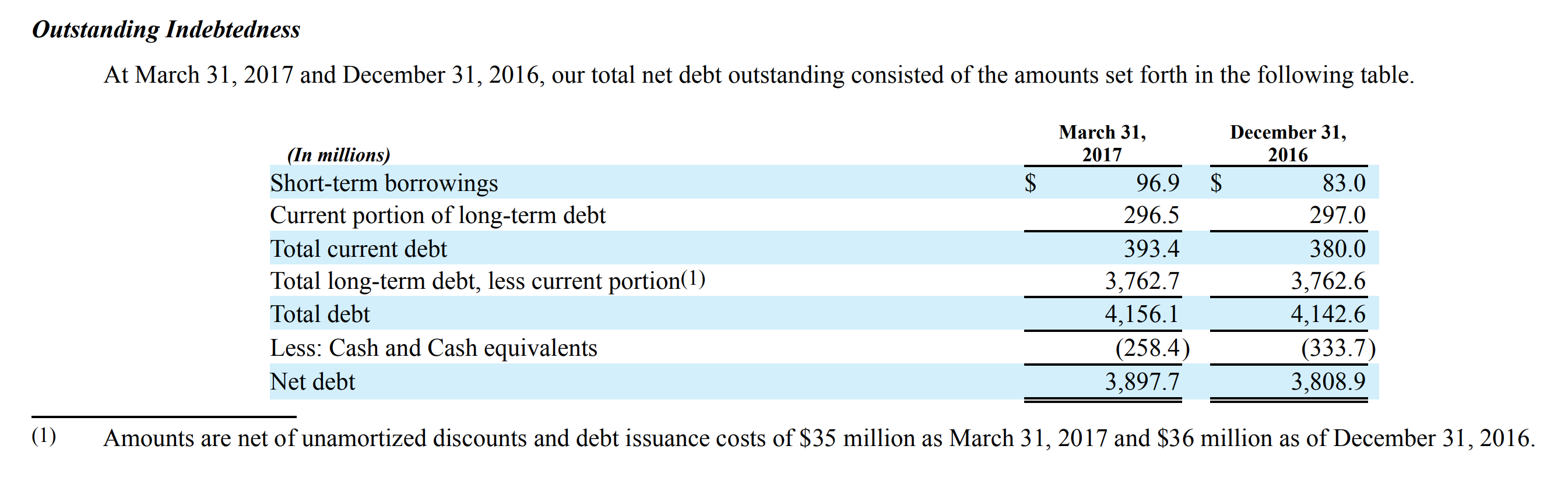

Companies will thus report debt figures on their balance sheet, net of debt issuance costs, as you see below for Sealed Air Corp:

This does not change the classification or presentation of the related amortization expense, which over the term of borrowing will continue to be classified within interest expense on the income statement:

Amortization of debt issuance costs shall be reported as interest expense

Source: FAS ASU 2015-03

The update impacts both private and public companies and applies to term loans, bonds and any borrowing that has a defined payment schedule. Below is an example of debt issuance costs treatment pre- and post-ASU 2015-03.

A company borrows $100 million in a 5-year term loan and incurs $5 million in financing fees. Below is the accounting at the borrowing date:

Below are the journal entries laid out explicitly over the next 5 years:

The changes prescribed under ASU 2015-03 for debt issuance costs associated with term loans and bonds do not apply to commitment fees paid to revolving credit lenders and are still treated as a capital asset. That’s because FASB views the commitment fee as representing the benefit of being able to tap the revolver in the future, as opposed to a third-party related fee with no discernible long-term benefit. That means that commitment fees continue to be capitalized and amortized as they have been in the past.

The purpose of the change is part of a broader effort by FASB to simplify its accounting rules. The new rules now align with FASB’s own rules for debt discounts (OID) and premiums (OIP) as well as with IFRS treatment of debt issuance costs. Prior to the update, debt issuance costs were treated as an asset while debt discounts and premiums directly offset the associated liability:

The Board received feedback that having different balance sheet presentation requirements for debt issuance costs and debt discount and premium creates unnecessary complexity.

– Source: FAS ASU 2015-03

Conceptually, since debt issuance fees provide no future economic benefit, treating them as an asset prior to the update conflicted with the basic definition of an asset:

Additionally, the requirement to recognize debt issuance costs as deferred charges conflicts with the guidance in FASB Concepts Statement No. 6, Elements of Financial Statements, which states that debt issuance costs are similar to debt discounts and in effect reduce the proceeds of borrowing, thereby increasing the effective interest rate. Concepts Statement 6 further states that debt issuance costs cannot be an asset because they provide no future economic benefit.

– Source: FAS ASU 2015-03

The change also aligns US GAAP with IFRS in this regard:

Recognizing debt issuance costs as a deferred charge (that is, an asset) also is different from the guidance in International Financial Reporting Standards (IFRS), which requires that transaction costs be deducted from the carrying value of the financial liability and not recorded as separate assets. – Source: FAS ASU 2015-03

Those that are involved in modeling M&A and LBO transactions will recall that prior to the update, financing fees were capitalized and amortized while transaction fees were expensed as incurred.

Going forward, transaction professionals should take note that there are now three ways that fees will need to be modeled:

So much for simplifying things. For what it’s worth, FASB did consider expensing the financing fees, aligning the treatment of financing fees with transaction fees, but decided against it:

The Board considered requiring that debt issuance costs be recognized as an expense in the period of borrowing, which is one of the options to account for those costs in Concepts Statement 6. …The Board rejected the alternative to expense debt issuance costs in the period of the borrowing. The Board concluded that this decision is consistent with the accounting treatment for issuance costs associated with equity instruments as noted in the preceding paragraph.

– Source: FAS ASU 2015-03

Effective December 15, 2015, FASB changed the accounting of debt issuance costs so that instead of capitalizing fees as an asset (deferred financing fee), the fees now directly reduce the carrying value of the loan at borrowing. Over the term of the loan, the fees continue to get amortized and classified within interest expense just like before. The new rules don’t apply to commitment fees on revolvers. As a practical consequence, the new rules mean that financial models need to change how fees flow through the model. This particularly impacts M&A models and LBO models , for which financing represents a significant component of the purchase price. While ignoring the change has no cash impact, it does have an impact on certain balance sheet ratios, including return on assets.

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.